If you’ve been trying to figure out where to put your retirement savings, you’ve probably run into three different account types: the traditional 401(k), Roth IRA and the Roth 401(k). All three help you build wealth for the future, but they work differently. The best choice for you depends on your income, unique tax situation, and where you are in your financial life.

The good news: for most people, the answer isn’t choosing just one. It’s understanding how each account works so you can use them strategically together.

Start Here: Maximize Your Employer Match First

Before comparing account types, there’s one step that comes first, regardless of which accounts you choose.

If your employer offers a 401(k) match, the first priority is always to contribute at least enough to capture the full match. Most employers match a percentage of what you contribute- for example, 50% of contributions up to 6% of your salary. That’s ‘free’ money added directly to your retirement savings, and it’s one of the highest-return moves available in personal finance.

Once you’re capturing the full match, the next question is: where should additional funds go? Whether that’s increasing your 401(k) contributions, opening an IRA, or directing money to a taxable brokerage account, this is where working with your financial planner and CPA to look at your specific financial picture can be a great choice.

The Core Difference: When You Pay Taxes

All three accounts’ main point of difference is tied to taxes.

Traditional 401(k): Pay Taxes Later

Contributions are pre-tax, reducing your taxable income today. Withdrawals in retirement are taxed as ordinary income.

Roth IRA: Pay Taxes Now

Like the Roth 401(k), contributions are made with after-tax dollars, and qualified withdrawals in retirement are tax-free. The key difference is where the account lives and who can contribute- more on that below!

Roth 401(k): Pay Taxes Now

Contributions are made with after-tax dollars- no deduction today. In exchange, qualified withdrawals in retirement are completely tax-free.

The question to ask yourself: Do you think your tax rate will be higher now or in retirement? If higher now- the traditional 401(k) deduction is more valuable. If higher later- the Roth accounts’ tax-free growth wins. If you’re uncertain, talk to your financial planner. If you don’t have one, we’d love to have an initial call to see if we’re a fit.

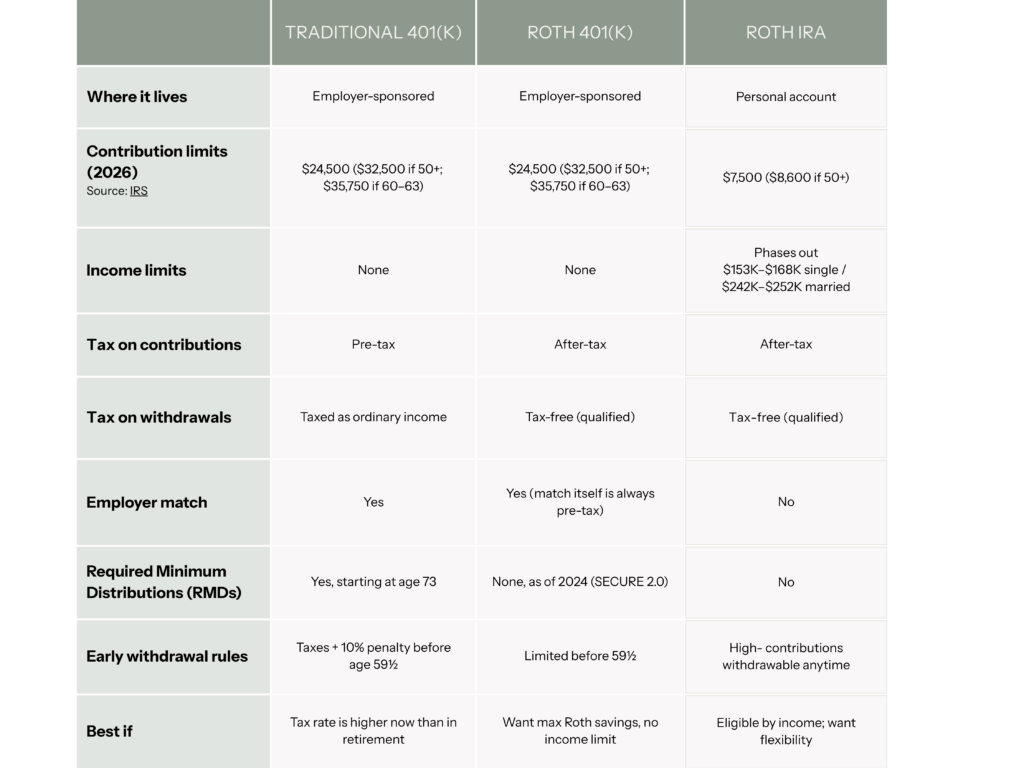

401k vs Roth IRA vs Roth 401k

Side-by-Side Summary

A few things worth highlighting beyond the table:

The Roth 401(k) has no income limit, which makes it the primary path to Roth savings for high earners who are phased out of the Roth IRA. And as of 2026, anyone with FICA wages over $150,000 in the prior year must make their catch-up contributions on a Roth basis- if your plan doesn’t offer a Roth option, you won’t be able to make catch-up contributions at all. That’s definitely worth flagging to your CFP® and CPA if this applies to you.

My Method: Think About Priorities

For most people, the order looks like this:

- Capture the full employer match in your 401(k)- traditional or Roth, doesn’t matter yet.

- Decide traditional vs. Roth for additional 401(k) contributions, based on whether you expect a higher or lower tax rate in retirement.

- Add a Roth IRA if you’re eligible- it offers more investment flexibility and easier access to contributions if needed.

- If you’re above the Roth IRA income limits, a backdoor Roth IRA is worth a conversation with your CPA: a non-deductible traditional IRA contribution converted to Roth. It’s not a do-it-yourself move- the rules get complicated if you hold other pre-tax IRA balances- but it can add another source of tax-free savings once the 401(k) options are maximized.

Why This Matters Beyond This Year’s Taxes

The value of using these accounts together is tax diversification: having pre-tax, Roth, and flexible savings to draw from strategically in retirement. When all your savings are pre-tax, every withdrawal is taxable income, which can push you into higher brackets, raise Medicare premiums, and increase how much of your Social Security is taxed.

A mix of account types gives you room to manage that each year- which is also one of the key factors in how long your retirement savings will last.

These are the types of decisions that benefit from a CFP® who coordinates directly with your CPA- not just deciding which accounts to use, but how they work together.

Ready to Build a Tax-Smart Retirement Plan?

At Method Financial Planning, we help busy families and pre-retirees think through exactly these kinds of decisions in the context of your actual income, goals, and timeline.

Schedule a free discovery call and take the first step toward a retirement plan that’s built around your life.